Happy Halloween to the VoLo Earth community!

As many of you know, metals are indispensable to the energy transition, serving as critical inputs across electric vehicles (EVs), renewable energy generation, and energy storage. As demand in these sectors surges, the metals supply chain faces mounting pressures to adapt.

Historically, metals and mining have been inextricable; mining has been the primary method of sourcing metals for thousands of years. While mining will continue to play a central role in the global economy and the energy transition, this relationship is shifting - and, in some cases, beginning to decouple.

Geopolitical Forces, Demand, and Import Dependencies

Geopolitics is a major force driving this evolution. As deglobalization accelerates and global trade and general alliances continue to shift in response to conflict, securing critical mineral supply has become paramount to national agendas across borders and political lines. The onshoring of supply, general reimagination of supply chains, and advancement of metal and mining technologies has become central to questions of national security and independence.

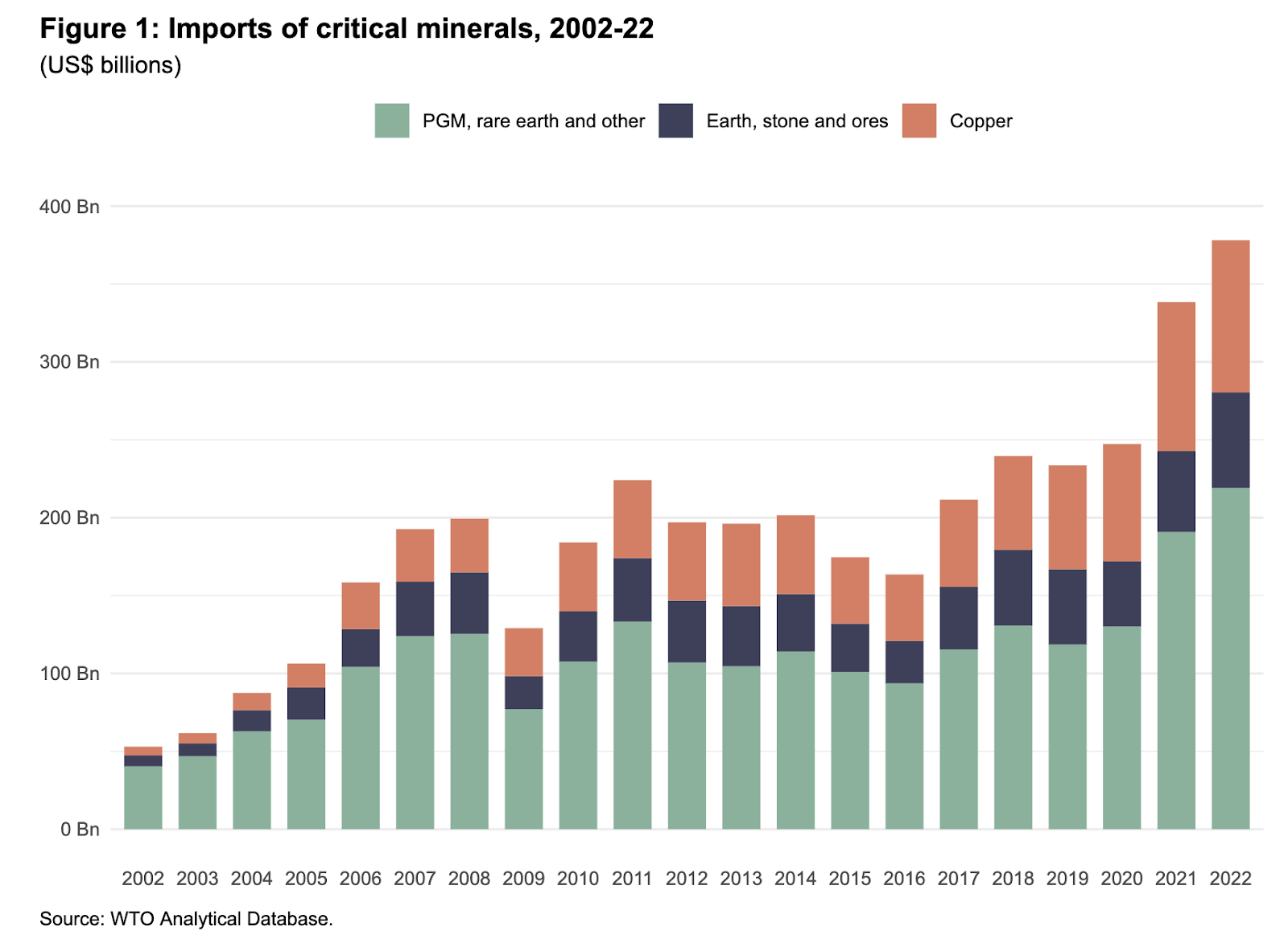

Metal imports shed light on this issue. The WTO reports that imports of critical metals surged from $53 billion in 2002 to $378.1 billion in 2022 - a sevenfold increase:

This growth reflects a sharp increase in metals demand and also underscores the geopolitically charged nature of the metals supply chain. As we observe this shift, we see a similar trend in the rising value of other strategic metals, like gold, which has recently surged to record highs as shifting global alliances and trade concerns inspire a focus on alternatives to national currencies.

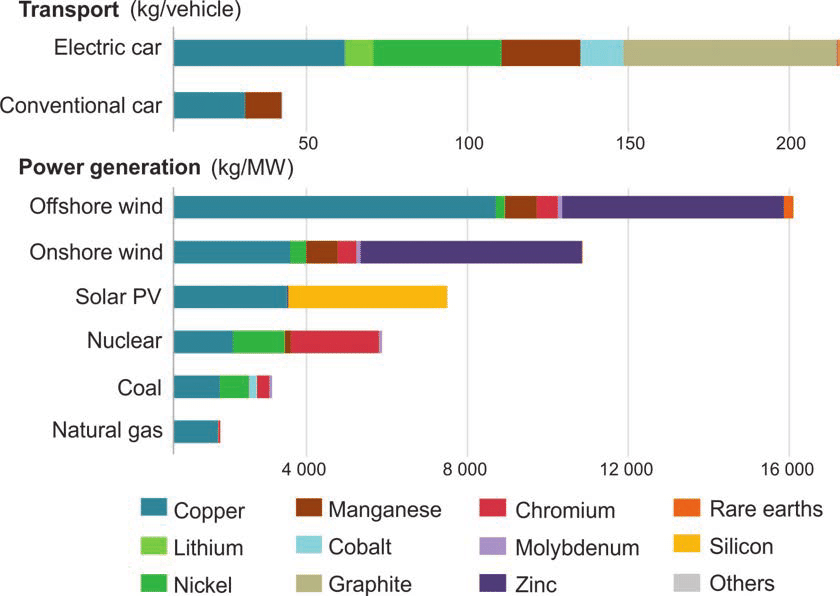

The energy transition lies at the cross-hairs of metal supply and demand. The energy transition is powering a significant rise in demand for critical metals. According to the IEA, a typical electric car requires six times the mineral inputs of a conventional car, and an offshore wind plant requires 13 times more mineral resources than a similarly sized gas-fired plant.

Meanwhile, since 2010, the average mineral resources needed per unit of new power generation capacity have risen by 50% as renewable investments expand, driving home the scale of demand disruption.

The chart below highlights the stark contrast in metal inputs required for fossil fuel-based versus renewable energy systems.

The need to address supply constraints - and even rethink supply - is evident.

Pathways of Supply Innovation

Responses to the ‘Supply question’ can be broadly categorized into three buckets: 1) Increase the efficiency of traditional supply, 2) Make better use of existing supply (reduce or circumventing pressure to generate new supply), or 3) Seek new sources of supply.

Naturally, there are innovations which cross-cut these categories. We will highlight an example pathway within each approach below:

Increase the efficiency and output of natural supply

Pathway example: Exploration Technologies - KoBold Metal and Earth AI

This includes advanced tools for locating and assessing mineral deposits, including satellite imaging, geophysical surveys, and geochemical analysis. Increasingly, AI and ML are beginning to revolutionize how companies discover new deposits of critical minerals by allowing a deeper view into the Earth’s subsurface to identify new ore bodies that were previously undetectable.

Key examples include KoBold Metals, whose discovery platform identified one of the largest copper deposits in over a century, as well as Earth AI. Earth AI similarly discovered the first nickel, PGE, and copper deposits in Australia (including the first identified igneous PGE-nickel-copper mineralization in the region).

Make better use of existing supply

Pathway example: EOL Critical Mineral Recovery - Nth Cycle

This includes technologies focused on recovering high-value critical metals from end-of-life products to reduce reliance on new mining.

Recent progress in metal recycling has demonstrated the economic potential of metal circularity, drawing substantial investment. Techniques include hydrometallurgy (aqueous extraction), pyrometallurgy (high-temperature processes), electro-extraction, biometallurgy (microorganism-driven), and tailings repurposing (i.e. BHP’s tailing challenge).

VoLo Earth portfolio company Nth Cycle is a key player, with electro-extraction technology demonstrated to recover up to 95% of critical minerals from discarded batteries. Nth Cycle’s Ohio facility, whose ‘groundbreaking’ ribbon-cutting was highlighted in last month’s newsletter, showcases that recycling operations can scale to provide a reliable stream of the high-quality nickel and cobalt essential for next-gen batteries. These kind of advances in end-of-life mineral recovery can dislocate the emphasis on traditional raw material extraction and redirect focus toward enabling circular supply models.

Establish new sources of supply

Pathway example: Metals without Mining - Magrathea Metals

As highlighted in the introduction, the concept of “metals without mining” represents an emerging frontier in the effort to onshore critical metal supply.

Magnesium is a key example, with a supply chain heavily reliant on China, which produces over 90% of the world’s magnesium, followed by Russia as the second-largest supplier. In addition to geopolitical implications, current extraction methods are also highly carbon-intensive. This combination occasions a leapfrog of traditional processes to novel and more resilient sourcing solutions. The opportunity is large, as magnesium embeds an ability to displace various applications of both steel and aluminum - at 75% lighter than steel and 33% lighter than aluminum, increased strength to weight ratios, higher thermal conductivity and corrosion resistance.

Magrathea Metals is addressing this gap by pioneering a new approach: extracting magnesium from brine (rather than mined ore) to provide the first domestically sourced magnesium in the United States in over 40 years. By tapping into a previously underutilized resource, Magrathea’s process enhances U.S. supply resilience and creates a reliable stream of lightweight magnesium essential for the energy transition.

Implications on Capital Flows

The evolving metals supply landscape is beginning to transform capital flows, with critical metals like lithium, nickel, cobalt, and magnesium shifting from commodities to strategic assets on the global balance sheet. Batteries, for example, are increasingly seen as assets with trade potential and resale value rather than one-time expenses. In Europe, export restrictions on used batteries and black mass underscore the shift, as these resources gain strategic importance for energy security and resilience.

This revaluation has drawn hedge funds and trading firms into metals markets, responding to the marrying of heightened demand with supply volatility and geopolitical risks. Meanwhile, national policies prioritizing supply resilience are further incentivizing investment into onshoring and resource innovations, redirecting VC capital toward startups focused on advanced recycling, circular supply models, and alternative sourcing.

As a result, defense funding has emerged as a new capital source, with national security and climate goals aligning around metals as critical to energy independence and resilience.

Meanwhile, products and services are emerging around new metal supply. For example, Minespider is a traceability and metal sustainability platform creating digital Product Passports to enable visibility across the metal supply chain.

Conclusion

Metals are not only critical resources but foundational assets reshaping supply chains, capital markets, and the energy transition. The future of critical metals supply depends on an integrated approach: expanding domestic production, advancing recycling technologies, and reimagining new sources, while balancing imports with geopolitical resilience. Each of these pathways reflects the broader dynamics driving the energy transition—a nexus for national security, defense, manufacturing, and economic development.

As demand for metals accelerates, supply landscapes are transforming rapidly. Breakthroughs in AI, battery chemistry, and even subsurface intelligence for applications like geothermal and hydrogen are steepening the innovation curve, building a resilient, adaptable supply chain capable of fueling the energy transition and supporting a shifting global economy.

VOLO EARTH COMMUNITY

We held our AGM in early October amidst Colorado's stunning peak foliage, making the perfect backdrop for insightful discussions and collaborative programming. After a productive day, we brought our partners into the mountains to unwind, connect, and enjoy the season’s beauty together.

We even caught the aurora borealis:

A heartfelt thank you to everyone who joined us and shared your perspectives. Your energy and ideas made these days truly memorable.

On another community note, we are thrilled to introduce two new VoLo Earth team members, Nicole Lombardo (Venture Partner) and Martin Whittaker (Advisor).

Nicole began collaborating with Kareem at SolarCity over 15 years ago, and continued building her career at Google as Principal of Climate & Energy. Nicole’s experience additionally includes roles at industry giants including Oracle and Intel. She brings a wealth of expertise in product strategy, go-to-market and business development in the industry to our team and portfolio.

Martin is a pioneer in the industry whose career has resulted in recognition including the 2020 NACD Directorship 100 list of influential people in corporate governance and Business Insider's 2020 list of 100 People Transforming Business. Most recently, Martin was the founding CEO of JUST Capital, where he leads efforts to drive private sector action on societal challenges. His diverse career spans leadership roles at Sonen Capital, MissionPoint, Swiss RE, and Innovest Strategic Value Advisors.

We are humbled to have these two on board, and so excited about the impact they are already bringing.

PORTFOLIO

Battery Materials Innovation

Sepion, a “leader in battery materials innovation” received a $17.5M grant from CALSTART and the California Energy Commission to build a cutting-edge lithium-ion battery separator manufacturing facility.

As a perfect conduit to the introduction letter above, Sepion’s ambition for the facility is to address the domestic battery separator supply gap. As Business Wire put it, Sepion’s new facility will initially produce “50 tons of its proprietary polymer and 50 million square meters of coated separator annually - enable to power 50,000 electric vehicles.”

Next Generation Power Transfer

Daanaa won 2024 BC Company of the Year for the startup category! The award recognizes companies and individuals who have made a significant impact on BC’s tech industry.

Daanaa was also highlighted as the example of an innovator poised to “significantly reduce time to market and production costs” for the EV market.

The article highlights how Daanaa’s solutions specifically target major challenges for EV manufacturers: speeding up time to market and lowering production costs by combining power functions into one step.

The Operating System for Concrete

Last month we shared news on the close of AICrete’s latest financing. A few weeks later, AICrete unveiled AggSense, an AI-powered sensor that delivers unprecedented operational intelligence for construction materials producers.

With seamless integration into AICrete’s operating system, AggSense provides contactless, real-time analysis of concrete aggregate properties (with levels of granularity including factors like particle size distribution and moisture content.) The sensors eliminate the need for traditional time-consuming tests and enable onsite calibration, with automatic AI updates pushed remotely. We are almost as eager as AICrete’s many customers to see the platform in action on the field.

Industrial Heat Decarbonization

Skyven and Western New York Energy (WNYE) announced a partnership to deploy the United States’ first-ever industrial steam generating heat pump.

A few months ago we highlighted Skyven’s breakthrough $145M non-dilutive DoE funding; the current announcement on WNYE is a preview of how Skyven is utilizing this funding to accelerate scale into the market.

READING

@VoLoEarth: The article highlights an often unrecognized fact that the Defense Department is the United State’s single largest energy customer (and also one of the largest energy consumers in the world). As we hinted towards in the opening letter, this dynamic promotes a differentiation between energy transition startups and traditional "climate tech" startups.

Energy transition companies have an opportunity to access a pool of growth capital (often non-dilutive capital) - through defense applications, which other segments of 'climate tech' may not. For example, the article discussed how the Pentagon's growing focus on energy security allowed EGS (Enhanced Geothermal Systems) startups like Sage Geosystems and Fervo Energy to secure significant defense contracts. We are optimistic that XGS (Fund II) is on a similar trajectory. We've already seen this play out in the portfolio in material ways; for example, Magrathea in Fund II, and Ion Storage Systems in Fund I, have both received meaningful non-dilutive capital from the US DoD.

@VoLoEarth: Plans to reopen and operationalize Three Mile Island over the next three years continue to grab headlines in the sector. Most recently, Constellation made a deal with Microsoft which intends for Three Mile Island to provide sufficient electricity to power the company’s data centers.

CTVC’s October take on Three Mile Island highlighted Amazon’s prioritization of speed. This echoes VoLo Earth’s May newsletter on the AI-Data Center Bubble, in which we disccused how “customers in a buying bubble are often prioritizing product attributes including speed of delivery and access to product over pricing. In other words, speed and scale shape price elasticity curves, creating a premium for rapid development.”

@VoLoEarth: McKinsey’s report highlights the expanding battery cell component market in Europe and North America, projecting rapid growth and increased local production demand as regions seek to reduce reliance on Asian suppliers.

With a $250 billion market potential by 2030, opportunities are ripe for new entrants to supply components like cathodes, anodes, separators, and electrolytes. This shift parallels rising investments in critical metal sourcing and aligns with government policies promoting supply chain security.

@VoLoEarth: Tapestry, Google X’s grid planning tool, announced deployment of its platform with Chile’s national grid operator (CEN). Tapestry will be used to support Chile’s annual transmission expansion planning process.

As the article highlights, “grid Planners have to anticipate what the grid might need to do every second of every day, years or even decades in advance. It’s heroes’ work and the job is getting harder each day as they juggle more dynamic renewables coming onto the grid, skyrocketing energy demands and a 100-plus-year-old-grid that wasn’t designed for today’s energy landscape.”

Tapestry provides a useful analog and market validation for the critical work Pearl Street is conducting with major operators in the US (such as MISO).

Tesla Announces Wireless Charging

@VoLoEarth: With Tesla's recent Robotaxi unveiling, and the announcement of wireless charging (above), many EV experts acknowledged the arguably inevitable solution for autonomous vehicles. "It's about high time we did this", stated Tesla's CEO Elon Musk. He's also publicly acknowledged that "Efficiency and Alignment" are the keys to making wireless charging successful.

VoLo Earth emphatically agrees, and our portfolio company HEVO focuses on these success factors. We are now seeing wireless peak efficiency from grid-to-battery higher than 93% (AC to DC) with new power electronics architecture and improved components. Electromagnetic designs have also become better, improving coil-to-coil transfer efficiency. HEVO's iterations of components and materials over the past five years is making wireless transfer just about as efficient as plug-in charging.